US Securities and Exchange Commission (SEC) Chairman Paul Atkins made news in March when he told an audience of securities industry professionals that change was on the way for Investment Advisers Act Rule 206(4)-5 (the Pay-to-Play Rule or the Rule). Atkins labeled the Rule “a trap for the unwary” and said that the SEC would address rule changes in 2026.1 While the nature and extent of regulatory changes the SEC may make to the Rule this year remain unclear, the existing Rule—together with myriad state- and local-level regulations—can impose draconian penalties on investment advisers based on particular types of political contributions.

This presents a heightened risk for investment advisers and their personnel in 2026 as dozens of current elected officials at the federal, state and local levels are running for a new office in the November election.

As many advisers are well aware, contributions to federal officials and candidates are typically not covered by the Pay-to-Play Rule. However, the Rule can apply to contributions to campaigns for federal office by current state or local officials, as well as contributions to campaigns for state or local office by current federal officials. Moreover, numerous state and local jurisdictions impose their own pay-to-play restrictions.

As contributions by certain types of investment adviser personnel to any one of these candidates present the potential for a pay-to-play violation, now is a good time for an investment adviser’s compliance and/or legal personnel to reinforce with employees the importance of complying with firm policies in connection with political contributions.

I. A Review of the Pay-to-Play Rule

Going into this busy election season, a refresher on the Pay-to-Play Rule is in order.2 The Rule was adopted by the SEC in 2010 to prevent investment advisers from using political contributions to improperly influence the award of state and local public investment pool advisory business. The Rule is intended to ensure that decisions regarding the selection of advisers to manage public investment pools such as state pension funds, public retirement systems, sovereign wealth funds and public higher education endowments are based on merit rather than on political donations.

To achieve this objective, the Rule prohibits an investment adviser from receiving compensation for providing advisory services to a state or local government entity for a two-year period if the adviser or one of its “covered associates”3 makes a political contribution to certain government officials4 or candidates for offices that can influence the selection of public investment pool investment advisers. This two-year prohibition, often referred to as the Rule’s two-year time-out, can apply even where the contribution is relatively small and there is no evidence that the contribution was intended to improperly influence the award of advisory business.

The Rule also contains a lookback provision, which can capture political contributions made before an individual becomes a covered associate. Contributions made within six months prior to an individual becoming a covered associate—or two years for individuals who will solicit government clients—may trigger the Rule once that individual assumes the covered role. And the Rule includes only limited exceptions. For example, a covered associate may make certain de minimis contributions without triggering the two-year prohibition.5 However, contributions exceeding these limits or contributions that otherwise fall within the scope of the Rule can lead to significant consequences.

Compliance with the Rule can be complex. First, the Rule’s definitions can be difficult to apply in practice. Determining whether an individual has “similar status or function” to an executive officer, whether an employee indirectly supervises a solicitor or whether a particular government official can influence adviser selection often requires analyzing complex organizational and governmental structures. Second, the Rule operates under a strict liability framework, meaning that a violation may occur even if the contributor had no intent to influence the selection of an investment adviser. Third, the consequences of even inadvertent violations can be significant.6 In addition to potential SEC enforcement actions and monetary penalties, the Rule may prohibit the adviser from receiving any compensation from the relevant government entity for a two-year period, which can have substantial commercial implications.

II. A Busy Election Season

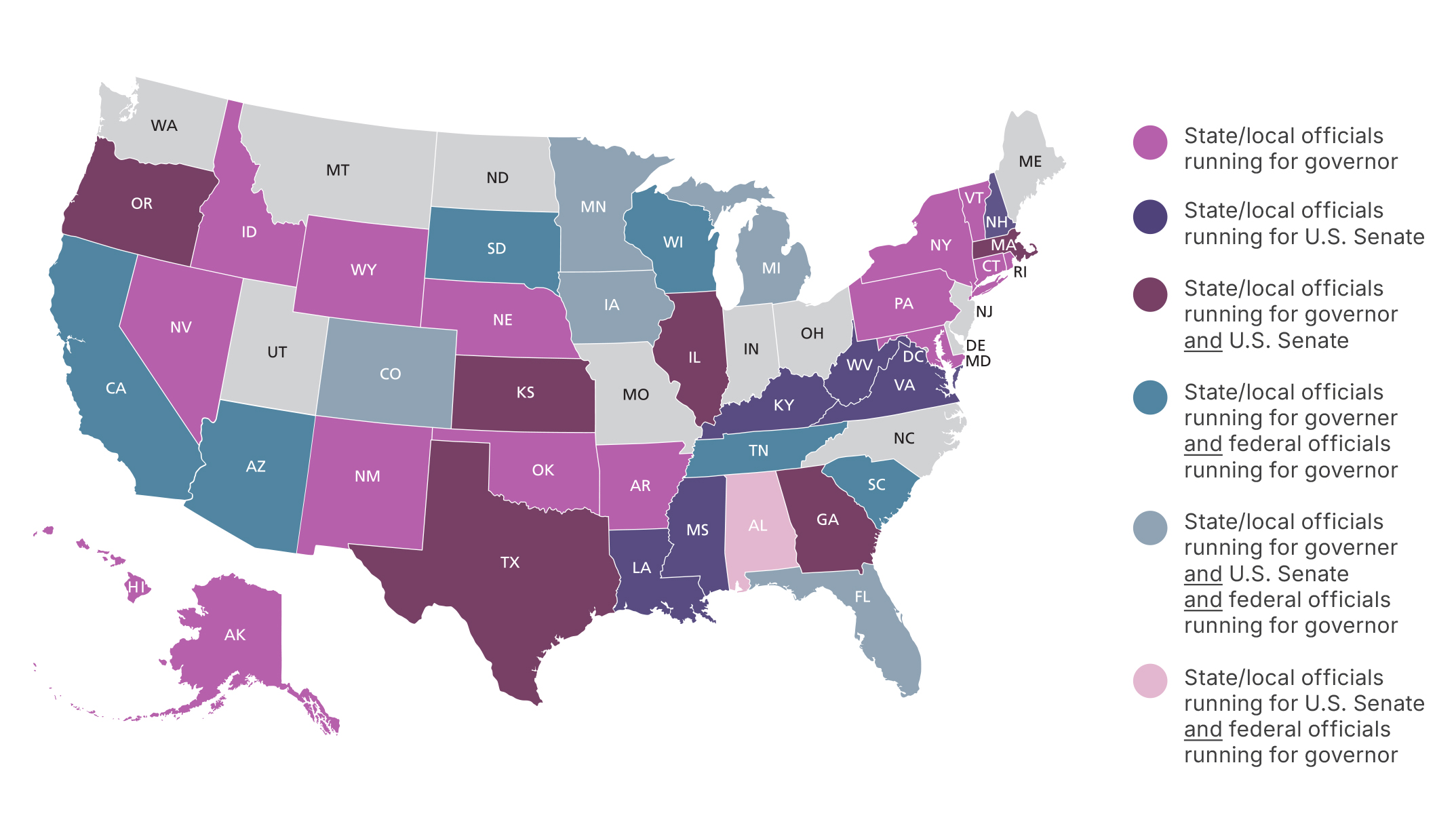

As noted above, dozens of current elected officials at the federal, state and local levels are running for a new office in 2026, a situation that presents a heightened risk for investment advisers and their personnel of inadvertent pay-to-play violations. As of the date of publication, there were 33 state and local elected officials running for US Senate and an even larger number running for the US House of Representatives, while 78 state and local elected officials and 15 federal elected officials are running for governor. The map below illustrates how widely this trend is distributed across the country.

Risk is heightened because, although the Pay-to-Play Rule primarily affects state and local elections, contributions to federal campaigns can also trigger the Rule when a candidate for federal office currently holds a state or local office. In those circumstances, contributions that might otherwise appear outside the Rule’s scope may create compliance exposure. For example, in a 2024 client alert, we highlighted how when Minnesota Gov. Tim Walz joined the Democratic presidential ticket, contributions to that campaign came under the Pay-to-Play Rule because the Minnesota governor sits on the Minnesota State Board of Investment, which oversees the selection of investment advisers for state investment funds. The same situation also applies in reverse; contributions to a current federal elected official who decides to run for a local or state office within the Rule’s definition of government official can trigger the Pay-to-Play Rule, even though the official’s role at the time of the contribution is a federal one.7

Because even relatively small contributions can lead to SEC enforcement, monetary penalties, and a two-year ban on compensation for investment advice provided to government clients, investment advisers reasonably impose strict controls on political contributions by covered personnel. As a result, election cycles involving large numbers of state and local officials running for federal office—and vice versa—can significantly increase the risk of inadvertent violations and warrant heightened attention from advisers’ compliance teams.

III. The Federal Rule Is Not the Only Consideration—State and Local Laws Apply Too

The Pay-to-Play Rule is only one part of the regulatory landscape. Numerous state and local jurisdictions impose their own pay-to-play restrictions that apply to entities seeking or holding government contracts or investment advisory mandates.

These rules often cover more categories of investment adviser affiliated campaign donors than does the federal concept of covered associates. For example, many state and local regimes apply to directors, officers, partners or significant owners of an investment adviser, and in some cases even to spouses, minor children or affiliated entities.8 The number and categories of individuals whose political contributions may trigger restrictions under state or local rules can therefore be much broader than those captured by the federal rule, requiring firms to monitor contributions across a wider group of personnel.

State and local pay-to-play rules also vary significantly in their structure and scope. Some jurisdictions impose outright prohibitions, preventing firms from receiving or being awarded government business for a defined period if certain political contributions are made.9 Other jurisdictions rely primarily on disclosure requirements, requiring firms and their principals to report political contributions made to covered officials or candidates.10

In addition, the covered offices and officials differ widely across jurisdictions. Some laws focus on officials responsible for awarding contracts or selecting investment advisers, while others cover a broader set of state-level or municipal offices, including governors, state legislators or members of boards overseeing public funds. The penalties for violations also vary, ranging from monetary penalties and disclosure violations to disqualification from government contracts or investment mandates.11

Because these requirements differ across jurisdictions, investment advisers must carefully evaluate political contribution activity against multiple regulatory regimes at once. Our WilmerHale team regularly assists clients in navigating these complexities, including mapping applicable state and local restrictions, implementing compliance controls and preclearance systems, and addressing potential violations or remediation efforts.